Eligibility and opening a Lifetime ISA

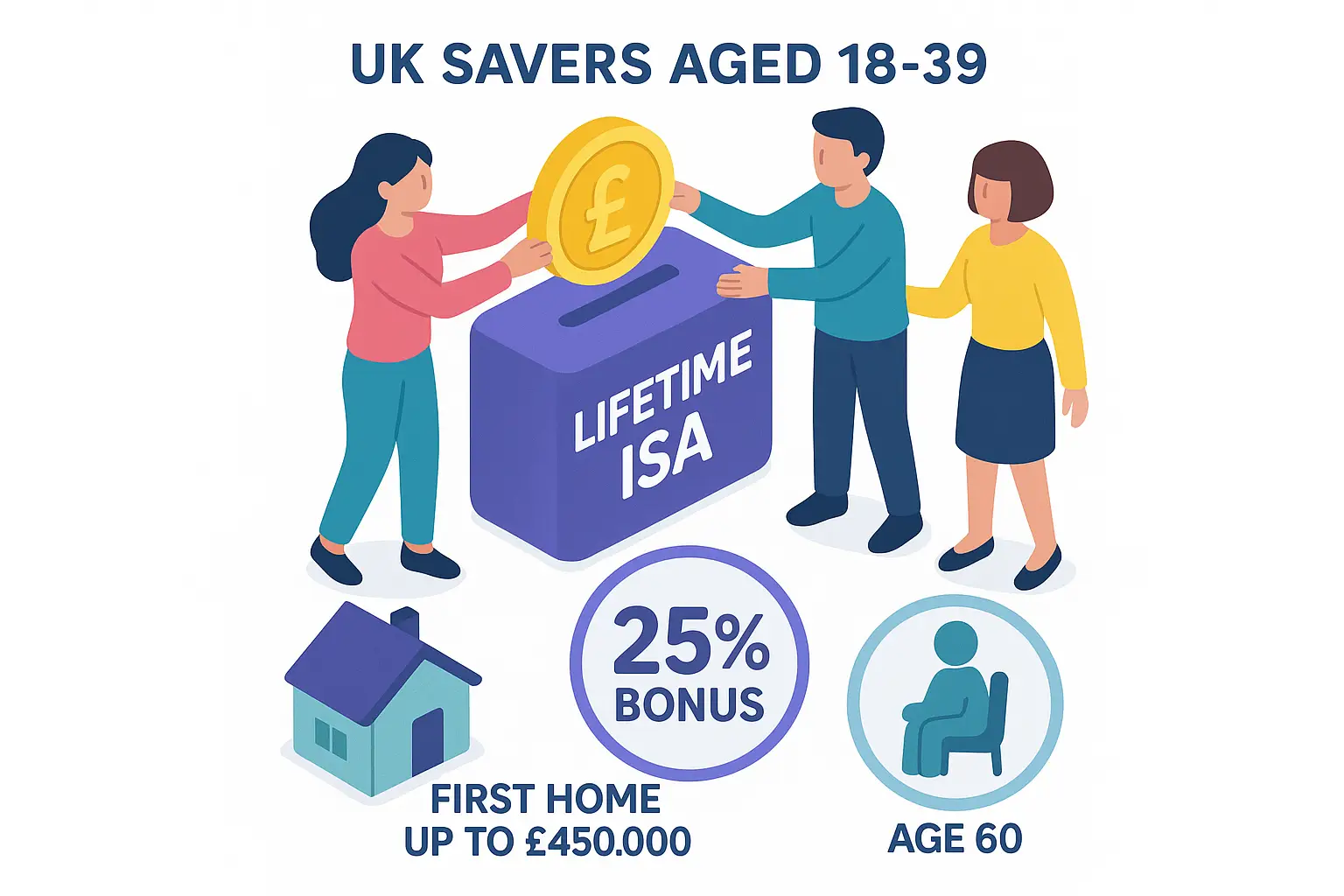

To open a Lifetime ISA (LISA), you must be a UK resident aged 18 to 39, and it’s designed primarily for first-time buyers or retirement savings. This lifetime isa rules uk setup ensures the scheme supports long-term goals like buying your first home or saving for later life.

Age and residency requirements

The core eligibility rule is that you can open a LISA between ages 18 and 39, with contributions allowed until you turn 50. You need to be a UK resident, meaning you live in the UK for tax purposes, as defined by HMRC guidelines on GOV.UK Lifetime ISA overview. If you’re under 18 or over 39, you won’t qualify, but once opened, the account remains active for tax-free growth.

First-time buyer criteria

As a first-time buyer under lifetime isa first time buyer rules, you must not have owned a residential property anywhere in the world before. This includes joint ownership, so check your status carefully if you’ve inherited or previously bought abroad. The rules tie into using LISA funds for a deposit on a home up to £450,000, helping young savers enter the property market.

Contribution limits and tax year rules

You can contribute up to £4,000 per tax year, which runs from 6 April to 5 April, and this forms part of the overall £20,000 ISA allowance. Lifetime isa deposit rules cap your annual input at this amount to qualify for the bonus, so plan contributions wisely to maximise benefits without exceeding limits. For 2025, no changes to the isa limit 2024 figures have been announced, keeping it steady at £4,000 for LISAs.

Tip: Before opening, verify your eligibility on GOV.UK to avoid issues later. Consider your long-term plans, as lifetime isa age rules lock in commitments early.

Government bonus and how it works

The government adds a 25% bonus on your contributions up to £4,000 annually, turning £4,000 into £5,000 instantly. This lifetime isa bonus rules incentive boosts savings for home purchases or retirement, but only applies to eligible deposits.

Bonus calculation and payment

For every £1 you save, the state contributes 25p, paid directly into your account by your provider within 30 days of contribution. The maximum bonus is £1,000 per year on £4,000 saved, as per official rules. This applies regardless of whether it’s a cash or stocks and shares LISA.

Qualifying contributions

Only new money counts towards the bonus; transfers from other ISAs don’t qualify. Contributions must be made before age 50, aligning with lifetime isa rules for sustained saving. Use a what is a lifetime isa guide to understand basics before depositing.

| Rule | Details |

|---|---|

| Eligibility | UK residents aged 18-39; contributions to 50 |

| Annual contribution | Up to £4,000 per tax year |

| Government bonus | 25% on contributions, max £1,000/year |

| Withdrawal conditions | Tax-free for first home ≤£450,000 or age 60+ |

| Penalties | 25% charge on unauthorised withdrawals |

Withdrawal rules and penalties

You can withdraw tax-free for a first home up to £450,000 or after age 60; otherwise, a 25% penalty applies to recover the bonus plus your savings. Lifetime isa withdrawal rules protect the scheme’s purpose but have drawn criticism for rigidity.

Permitted withdrawals (home purchase and retirement)

For home buying, funds must go towards a deposit within 90 days of completion, limited to £450,000 property value under lifetime isa first home rules. At 60 or older, full tax-free access is allowed for any purpose. Small non-penalty withdrawals are possible for emergencies, but only your own contributions without the bonus.

Unauthorised withdrawal charges

Breaking lifetime isa rules triggers a 25% charge on the entire withdrawal, including growth and bonus, effectively clawing back the government’s input plus extra. As explained in GOV.UK withdrawal rules, this can leave you worse off than starting. What happens if you break lifetime isa rules? You lose the bonus equivalent and face an additional hit.

Recent penalty statistics

In 2024/25, Lifetime ISA penalties totalled £102 million, affecting nearly 100,000 savers, up from £75 million the prior year (The Independent, 2025). This lifetime isa penalty withdrawal trend highlights rising use but also cautionary tales. HMRC data shows the charge often exceeds the bonus gained.

Transfer and contribution rules

Transfers to another LISA are allowed but count towards your annual £4,000 limit, with no government fee but possible provider charges. Lifetime isa transfer rules ensure continuity without losing tax benefits.

Transferring between providers

Instruct your current provider to transfer to a new one; it must be a LISA to preserve status. This process, detailed on GOV.UK, takes up to 30 days and qualifies for bonus if within limits. Explore lifetime isa providers for options.

Annual allowance details

Your £4,000 LISA limit is separate from other ISAs, allowing up to £20,000 total tax-free savings. Contributions reset each tax year, so time deposits accordingly. For rates, check best lifetime isa rates.

Combining with other ISAs

You can hold multiple ISAs, but LISA contributions are ring-fenced. This flexibility supports diverse saving strategies under overall isa rules.

Potential changes and criticisms of Lifetime ISA rules

No major lifetime isa rules change for 2025 has been confirmed, but discussions around penalty reforms continue amid backlash. Are lifetime isa rules changing? Watch for Budget updates.

2025 updates and speculation

The £4,000 limit and 25% bonus remain unchanged into 2025, per HMRC. Will lifetime isa rules change? Speculation focuses on house price thresholds, but nothing official yet (AJ Bell, 2024). Monitor AJ Bell withdrawal guide for insights.

Common criticisms and penalty issues

Lifetime isa rules criticism centres on the harsh 25% penalty, seen as punitive for life changes like job loss. Figures show £102 million in charges, sparking calls to scrap or soften it (GB News, 2025). This has led to debates on fairness for young savers.

Advice for savers

Assess your five-year horizon before committing, as penalties can erode gains. For the best lifetime isa, align with goals. Consult a financial adviser for personalised fit.

Frequently asked questions

What are the rules for withdrawing from a Lifetime ISA?

Under lifetime isa withdrawal rules, you can take money out tax-free if it’s for your first home purchase up to £450,000 or after age 60 for any reason. Otherwise, a 25% government charge applies to the full amount withdrawn, including your contributions, bonus, and growth, to discourage early access. This rule, as outlined on GOV.UK, aims to enforce long-term saving but has resulted in significant penalties for many users in recent years.

Who is eligible for a Lifetime ISA?

Eligibility for a Lifetime ISA requires you to be aged 18 to 39 and a UK resident, with the account usable for contributions until age 50. It targets first-time buyers or those saving for retirement, excluding anyone who has previously owned a home. These lifetime isa rules uk ensure the scheme supports specific life stages, but check your status via HMRC to confirm.

What is the Lifetime ISA bonus?

The Lifetime ISA bonus is a 25% government top-up on your contributions, up to £1,000 per year on a maximum £4,000 deposit. This lifetime isa bonus rules mechanism effectively boosts your savings instantly, making it attractive for home deposits or pensions. However, the bonus is clawed back via penalties if rules are broken, so understand the conditions fully before starting.

What happens if you withdraw from a Lifetime ISA before age 60?

If not for a qualifying first home buy, withdrawing before 60 incurs a 25% penalty on the entire sum, potentially leaving you with less than you put in. Lifetime isa withdrawal rules uk specify this charge recovers the bonus plus an extra 6.25% on your own money. In 2024/25, this hit over 100,000 savers for £102 million total, underscoring the risk of unplanned access.

Can you transfer a Lifetime ISA?

Yes, you can transfer a Lifetime ISA to another provider, but it must go to another LISA and counts towards your annual £4,000 allowance. Lifetime isa transfer rules prevent loss of tax-free status, with the process handled by providers and no direct government cost, though fees may apply. This flexibility helps switch for better rates without restarting your savings journey.

Are Lifetime ISA rules changing in 2025?

Currently, no confirmed changes to core lifetime isa rules for 2025, including the £4,000 limit and 25% bonus/penalty. However, ongoing criticism of penalties has prompted discussions, potentially leading to reforms post-Budget. Monitor official HMRC announcements, as are lifetime isa rules changing queries reflect saver concerns over rising house prices and economic shifts.

What are the penalties for breaking Lifetime ISA rules?

Breaking rules, like unauthorised withdrawals, results in a 25% charge on the withdrawn amount, as per lifetime isa penalty withdrawal guidelines. This not only recoups the government bonus but also penalises your principal, with 2024/25 seeing £102 million in total charges (The Independent). Expert strategy: Build an emergency fund outside the LISA to avoid this trap, and consider the scheme’s rigidity in volatile markets.