Understanding cash ISAs and current market rates

The best ISA rates in 2025 offer tax-free returns up to 4.51% AER for easy access cash ISAs, making them ideal for savers seeking flexibility without sacrificing yields. Cash ISAs provide a secure way to grow savings sheltered from income tax, with rates influenced by the Bank of England’s base rate and competition among providers. As of October 2025, top rates have stabilised post the 2022 hikes, but projections suggest slight declines if inflation eases further.

What is a cash ISA?

A cash ISA, or Individual Savings Account, is a tax-free savings product where interest earned remains exempt from UK income tax. Unlike regular savings accounts, cash ISAs protect up to £20,000 annually from taxation, appealing to higher-rate taxpayers. Providers like building societies and banks offer variants such as easy access for withdrawals anytime or fixed terms for guaranteed rates, all protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per institution.

2025 ISA allowance and tax benefits

For the 2025/26 tax year, the ISA allowance stands at £20,000, allowing savers to invest this amount across cash, stocks and shares, or innovative finance ISAs without tax on returns. This tax shield is crucial as basic-rate taxpayers pay nothing, while higher earners save up to 45% on interest. Subscriptions to cash ISAs rose 12.4% to £52.6 billion in the prior year, per HMRC data, highlighting their popularity amid rising living costs.

How rates are calculated (AER explained)

AER, or Annual Equivalent Rate, standardises interest comparisons by showing the effective yearly return, accounting for compounding. For example, a 4% nominal rate compounded monthly yields about 4.07% AER. This metric ensures fair evaluation of the best ISA interest rates, as variable rates may fluctuate while fixed ones lock in stability.

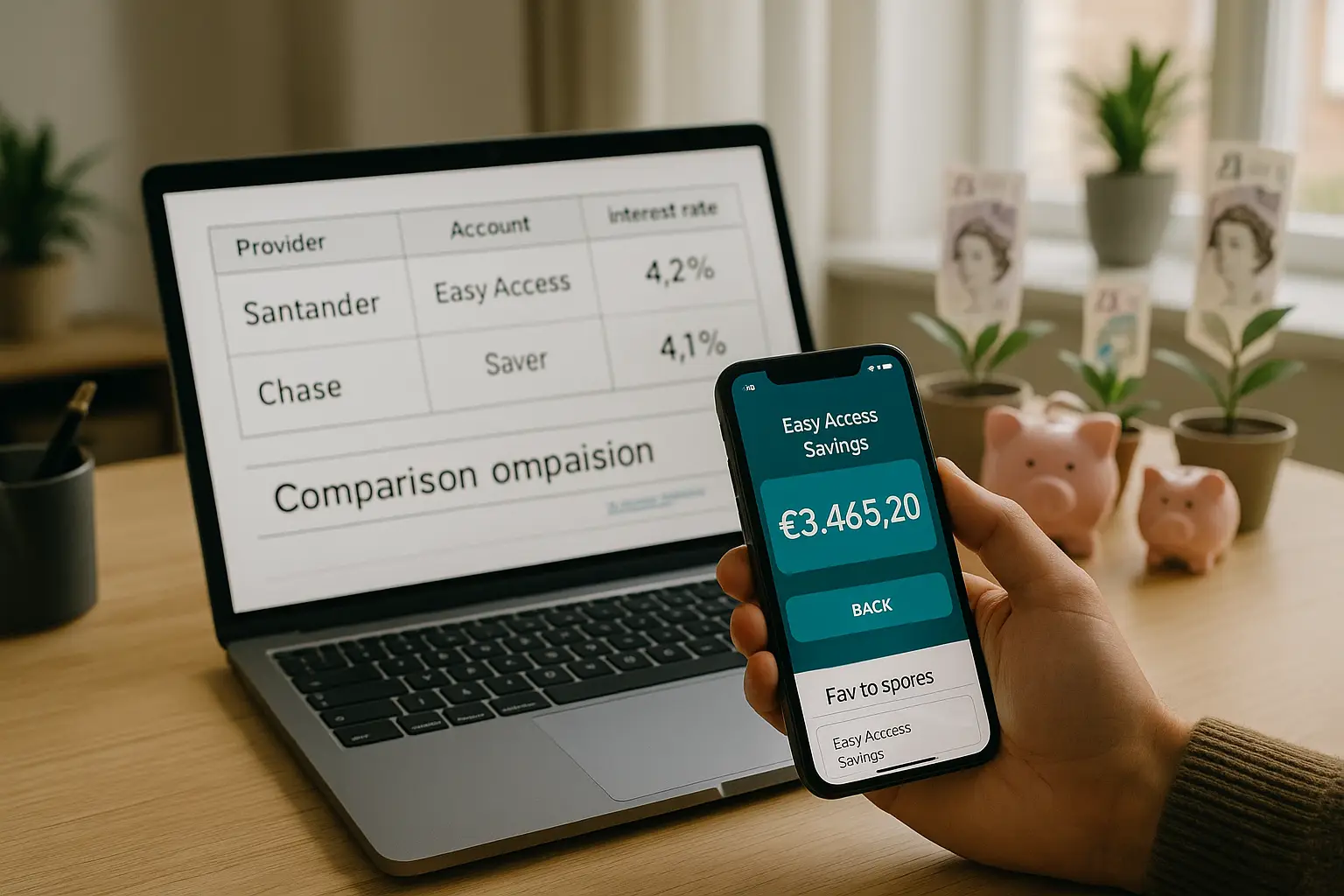

Top easy access cash ISA rates

The leading easy access cash ISA rates hit 4.51% AER as of September 2025, outperforming standard savings by offering instant withdrawals with competitive yields. These variable rates suit those needing liquidity, though they can change with market shifts. Providers compete fiercely, with top options from building societies edging out high-street banks.

Best overall easy access options

For maximum flexibility, the best cash ISA rates uk focus on no-notice withdrawals and minimum deposits from £1. Top performers include those from specialist providers, delivering 4.51% AER tax-free. Savers should prioritise FSCS protection and check for introductory bonuses that boost initial returns.

Rates for over 60s

Seniors enjoy preferential best ISA rates for over 60s, up to 4.16% AER on easy access products tailored for retirees. These often include higher starting balances or loyalty perks from banks like Halifax. According to Which?, such rates reflect customer satisfaction surveys, making them reliable for pension income supplementation.

Provider comparison

Compare the best easy access ISA rates below, based on data from leading comparison sites. This table highlights top contenders for 2025, focusing on accessibility and yields.

| Provider | Rate (AER) | Minimum Deposit | Access Type | Notes |

|---|---|---|---|---|

| Chip | 4.51% | £1 | Easy Access | App-based, variable |

| Moneybox | 4.45% | £500 | Easy Access | Digital provider |

| Plum | 4.40% | £100 | Easy Access | Flexible withdrawals |

| Trading 212 | 4.35% | £1 | Easy Access | Investment-linked |

| Virgin Money | 4.16% | £1 | Easy Access | Senior perks available |

Source: Moneyfacts Compare, accessed October 2025. Rates subject to change; verify eligibility.

Best fixed rate ISAs for 2025

Fixed rate ISAs guarantee up to 4.27% AER for one year, ideal for risk-averse savers betting on rate cuts ahead. These lock funds for stability, outperforming variables if base rates fall as forecasted. In 2025, short-term fixes dominate due to economic uncertainty.

1-Year fixed deals

The best 1 year fixed ISA rates reach 4.27% AER, with minimum deposits from £500. Providers like Shawbrook Bank lead, offering penalty-free early access in some cases. This term balances commitment with near-term liquidity needs.

Longer-term fixed rates

For two- to five-year horizons, rates dip to 3.80-4.00% AER, suiting long-term planners. Longer fixes protect against drops but penalise withdrawals heavily. Compare via MoneySavingExpert for the best fixed cash ISA rates.

Pros and cons of locking in

Pros include predictable returns and beating inflation at current levels. Cons: Illiquidity and potential opportunity cost if rates rise unexpectedly. Weigh against easy access if you anticipate needing funds soon.

- Pros: Tax-free certainty, higher initial yields.

- Cons: Penalties up to 180 days’ interest, no flexibility.

- Best for: Savers with emergency funds elsewhere.

Expert recommendations from Martin Lewis

Martin Lewis, via MoneySavingExpert, endorses the best ISA rates martin lewis picks, emphasising easy access at 4.51% for most. His advice prioritises tax efficiency and switching to top deals annually. For 2025, he warns of base rate volatility impacting yields.

MSE’s top picks

MSE highlights variable cash ISAs from Chip and Moneybox as winners, based on rigorous comparisons of over 50 providers. Fixed options from United Trust Bank score high for 1-year terms. Always check Lewis’s updates for timely alerts.

Advice for seniors and families

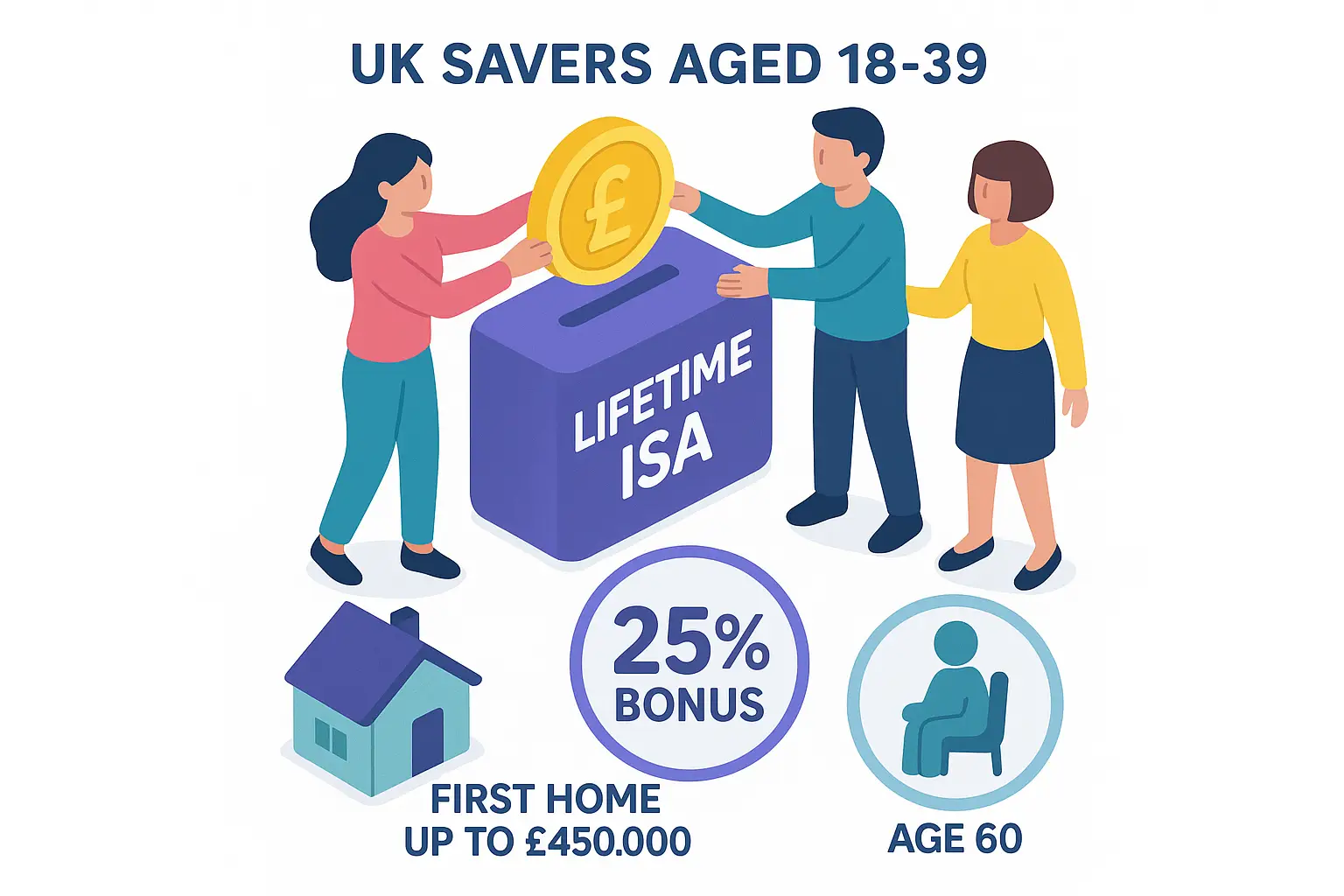

For over 60s, Martin Lewis best ISA rates for over 60s include boosted easy access from Virgin Money. Families should consider junior ISAs at 4.10% AER for child savings. Lifetime ISAs add a 25% government bonus for first-time buyers under 40.

Junior and lifetime ISA options

Best junior ISA rates offer 4.10% AER variable, with £9,000 annual allowance until age 18. Lifetime ISAs suit 18-39s saving for homes or retirement, matching contributions up to £1,000 yearly. These provide long-term tax-free growth beyond standard cash ISAs.

How to choose and switch ISAs

Select ISAs by matching access needs to rates: easy for flexibility, fixed for security. Switch via providers handling transfers seamlessly, preserving tax-free status. 2025 forecasts predict easy access at 4.00-4.20% if base rates hold.

Eligibility checks

UK residents aged 18+ qualify, with over-60s accessing seniors-only deals. Confirm FSCS coverage and no foreign tax issues. Use eligibility tools on provider sites.

Transfer process

Contact your new provider to initiate; they manage the old one, typically within 30 days. No tax lost, but avoid withdrawals to keep allowance intact. For guidance, review MSE’s transfer tips.

2025 rate forecasts

Experts project best ISA rates 2025 stabilising around 4% amid cooling inflation, per Moneyfacts analysis. Fixed terms may edge higher short-term. Monitor Bank of England announcements quarterly.

Provider spotlights and comparisons

Nationwide and Halifax offer competitive best cash ISA rates nationwide, with easy access at 4.00-4.20% AER. Building societies like Yorkshire BS provide superior fixed deals versus banks’ broader access.

Nationwide and Halifax rates

Nationwide’s easy access hits 4.10%, with £1 minimum; Halifax mirrors for seniors. Both ensure FSCS protection and app-based management. Compare via Nationwide’s tool.

Building societies vs. banks

Building societies yield 0.2-0.5% higher on average due to member focus, per Which? data. Banks excel in branch access and bundled perks. Choose based on convenience over marginal rate differences.

Avoiding common pitfalls

Don’t exceed £20,000 across ISAs or forget to transfer before deadline. Watch for teaser rates dropping post-intro. Regularly review to chase the best ISA savings rates.

Frequently asked questions

What is the best ISA for 2025?

The best ISA for 2025 depends on your needs, but top cash options like easy access at 4.51% AER from Chip suit flexible savers seeking maximum returns without locks. For stability, 1-year fixed ISAs at 4.27% AER offer guaranteed yields amid potential rate cuts. Consider your risk tolerance and access requirements, consulting MSE for personalised picks to optimise tax-free growth.

How much can I put in an ISA this year?

The 2025/26 ISA allowance is £20,000, split across cash, stocks, or lifetime types as you choose. This resets each tax year from 6 April, allowing fresh contributions without affecting prior balances. Exceeding it means taxable interest, so track via HMRC statements; unused allowance doesn’t carry over, urging full use for best ISA rates benefits.

What are the best easy access ISAs?

Best easy access ISAs deliver 4.51% AER tax-free, with providers like Moneybox leading for low deposits and no penalties. They provide liquidity for emergencies while beating inflation, unlike fixed alternatives. Compare via Moneyfacts for daily updates, ensuring FSCS cover up to £85,000 for security.

Are fixed rate ISAs worth it?

Fixed rate ISAs are worth it if you can lock funds and expect rates to fall, securing 4.27% AER for one year versus variable dips. However, penalties for early access make them unsuitable for short-term needs. For conservative savers, they outperform easy access long-term, but diversify if rates rise unexpectedly.

What ISA rates do over 60s get?

Over 60s access boosted best cash ISA rates for over 60s up to 4.16% AER on easy access from Halifax or Virgin Money, often with seniority perks. These reflect higher customer loyalty and lower risk profiles, per Which? surveys. Fixed options for seniors reach 4.00%, ideal for pension supplements without tax erosion.

Can I have multiple ISAs?

Yes, you can hold multiple ISAs from different providers, as long as total contributions stay under £20,000 yearly. This allows mixing easy access for liquidity and fixed for yields, maximising the best isa rates across types. Transfers between them preserve tax status, but avoid duplicates in one category to simplify management.

What are the best junior ISA rates?

Best junior ISA rates in 2025 offer 4.10% AER variable for under-18s, with £9,000 allowance managed by parents. Providers like Coventry Building Society lead, providing tax-free compounding until maturity. These build wealth securely, outperforming adult savings for family planning; review annually for switches.

How do fixed and easy access ISA rates compare in 2025?

In 2025, fixed ISAs edge easy access with 4.27% versus 4.51% AER initially, but variables offer flexibility amid forecasts of base rate stability. Fixed suits long-haul security, while easy access avoids penalties for retirees. Balance based on horizon: short-term favours variables, per MoneySavingExpert comparisons.