Understanding ISA types and benefits

Individual Savings Accounts, or ISAs, offer tax-free savings and investment options in the UK. For those searching for the best ISA rates, starting with the basics helps identify the right type. Cash ISAs are the most straightforward, providing interest without tax deductions.

What is a Cash ISA?

A Cash ISA is a savings account where interest earned is exempt from income tax and capital gains tax. It suits savers wanting security similar to a regular savings account but with tax advantages. You can deposit up to £20,000 annually, as confirmed for the 2025/26 tax year by Which? Providers like Nationwide and Virgin Money offer these, protected by the FSCS up to £85,000 per person.

Fixed vs easy access ISAs

Fixed rate ISAs lock your money for a set period, often yielding higher interest, such as up to 4.28% AER for one year according to Moneyfactscompare. Easy access ISAs allow withdrawals anytime but typically offer lower rates, like 4.51% AER for top easy access options from MoneySavingExpert. Choose fixed for stability if you won’t need the funds soon, or easy access for flexibility amid potential rate changes.

Junior and Lifetime ISAs

Junior ISAs help parents save for children under 18, with tax-free growth until age 18. Lifetime ISAs combine savings and investment for first home or retirement, with a £4,000 limit and government bonus. These specialized types expand beyond standard cash ISAs, targeting long-term goals.

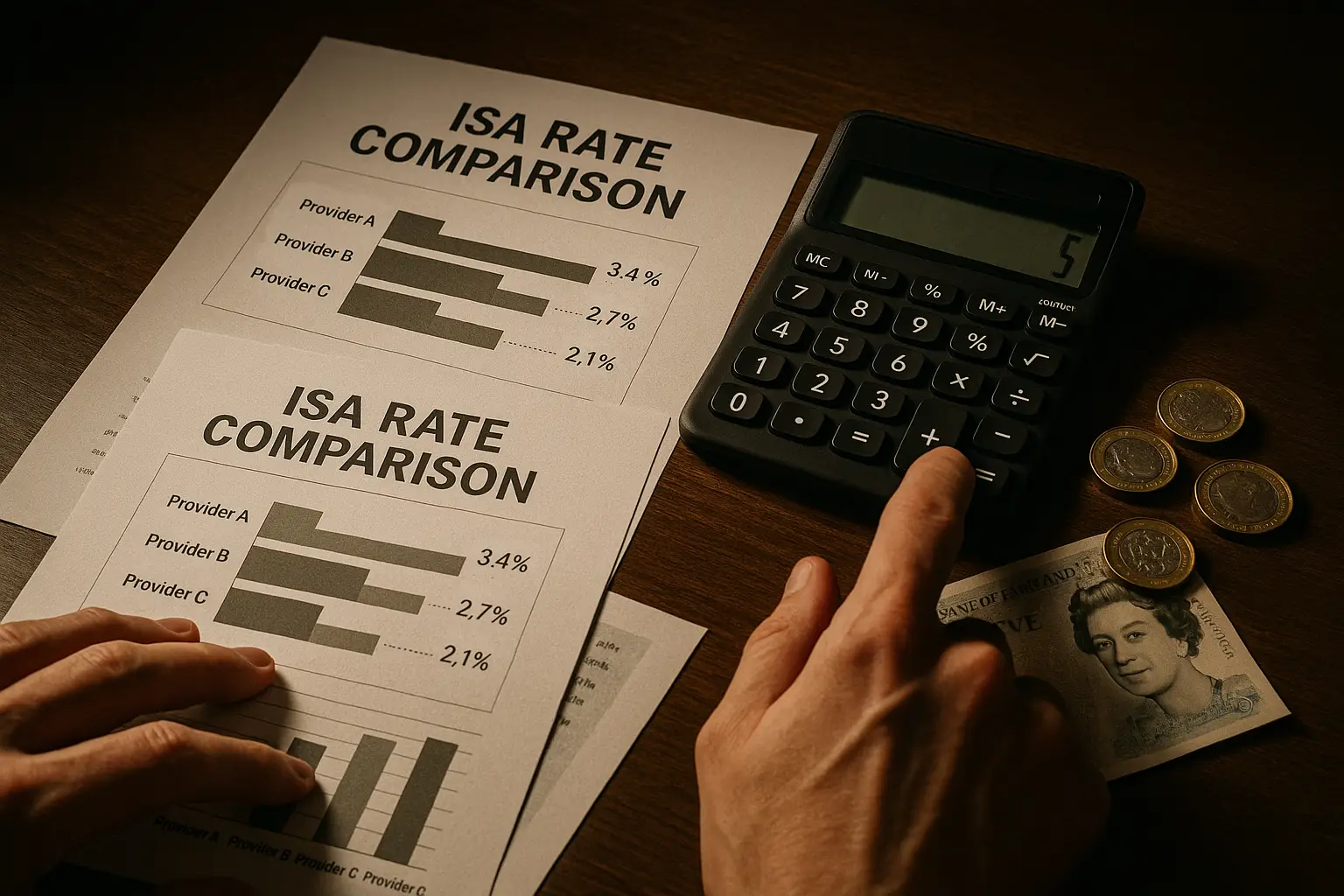

Top Cash ISA rates for 2025

The best cash ISA rates in the UK for 2025 hover around 4.5% to 4.9% AER, driven by Bank of England base rate influences. Providers compete fiercely, with top deals from building societies and online banks outperforming high street options. This section compares leading rates to help you secure the highest returns.

Best easy access rates

Top easy access cash ISA rates reach 4.51% AER as of October 2025, per MoneySavingExpert’s daily updates. For those prioritizing liquidity, these allow penalty-free withdrawals while beating inflation. Virgin Money and Coventry Building Society lead, offering competitive AER without minimum deposits.

Top providers and comparisons

| Provider | Rate (AER) | Type | Min Deposit | Access |

|---|---|---|---|---|

| Virgin Money | 4.51% | Easy Access | £1 | Unlimited |

| Coventry Building Society | 4.51% | Easy Access | £1 | Unlimited |

| Nationwide | 4.20% | Easy Access | £1 | Unlimited |

| Yorkshire Building Society | 4.92% | Fixed (1 year) | £10 | Limited |

This table draws from Moneyfactscompare data, highlighting the best ISA rates across types. Yorkshire Building Society edges out with 4.92% for fixed, while easy access leaders tie at 4.51%. Always check FSCS protection for safety.

How rates are calculated

AER (Annual Equivalent Rate) standardizes interest comparisons, assuming daily compounding. Rates factor in base rate decisions and competition; expect slight dips if inflation eases in 2025. Use comparison tools from sites like Moneyfactscompare for real-time figures.

best isa rates easy access options often include bonuses for new customers.

Best fixed rate ISAs

Fixed rate ISAs guarantee returns for terms from six months to five years, ideal for risk-averse savers. In 2025, the best fixed ISA rates start at 4.28% for short terms, per recent benchmarks. These outpace easy access amid stable economic forecasts.

1-year fixed options

The best 1 year fixed ISA rates hit 4.28% AER, locking in gains against potential cuts. Providers like Shawbrook Bank offer these with £1 minimums but early withdrawal penalties up to 180 days’ interest. Suitable if you have surplus cash post-emergency fund.

best isa rates fixed details provide deeper term analysis.

Longer-term rates

Two- to five-year fixed ISAs yield 4.0% to 4.5% AER, balancing commitment with returns. Longer locks protect against rate falls but tie up funds. Tembo highlights up to 4.92% for select longer deals.

Pros and cons

Pros include predictable earnings and higher yields; cons involve illiquidity and penalties. Weigh against your timeline—fixed suits medium-term savers. GOV.UK reports 25.3% LISA subscription growth in 2025, signaling demand for secure options.

ISA rates for over 60s

Seniors seek stable, accessible best ISA rates for over 60s, often with preferential terms. Martin Lewis best ISA rates for over 60s emphasize easy access to cover retirement needs. Rates mirror general offerings but with age perks like no-notice accounts.

Senior-specific deals

Best cash ISA rates for over 60s reach 4.2% AER on easy access, tailored for pensioners. Providers offer loyalty bonuses; check FSCS limits. These beat standard savings amid personal savings allowance caps.

best isa rates for over 60s guide explores eligibility.

Halifax and Nationwide options

Halifax provides 3.9% AER for over-55s on fixed one-year ISAs, while Nationwide’s Loyalty Saver hits 4.0% for seniors. Both UK high-street names ensure branch access. Compare via Which? for fees.

Tax considerations

ISAs shield interest from basic rate tax; vital as pensions may push brackets. Over 60s benefit most with larger pots. No changes for 2025/26 per FCA.

Best Junior ISA rates

Junior ISAs grow tax-free for children, with best junior ISA rates at 4.5% AER easy access. Parents can contribute £9,000 yearly. Focus on compounding for future education or homes.

Current top rates

Top providers like Coventry offer 4.51% AER; fixed options up to 4.3%. Junior cash ISA best rates emphasize safety over stocks.

Long-term savings tips

Start early for compound growth; diversify to Lifetime ISAs at 18. Avoid withdrawals to maximize tax-free status.

Provider guide

Nationwide and HSBC lead for juniors, with low mins. Review annually as rates shift.

How to choose and open an ISA

Select based on access needs, term, and rates; use £20,000 allowance wisely. Opening online takes minutes; compare first.

Eligibility and allowance

UK residents 18+ qualify; £20,000 limit per tax year (6 April-5 April). Unused rolls over unused.

martin lewis best isa rates tips aid decisions.

Switching providers

Transfer penalty-free within 30 days; platforms like Moneybox simplify. Consolidate for better rates.

2025 rate forecasts

Expect 4.0%-4.5% averages if base rate holds; track Bank of England. Best ISA rates 2025 UK may dip slightly but remain attractive vs inflation.

Frequently asked questions

What is the best easy access ISA rate in 2025?

The best easy access ISA rate for 2025 is 4.51% AER from providers like Virgin Money and Coventry Building Society, as per MoneySavingExpert updates. This rate allows flexible withdrawals, making it ideal for emergency funds or short-term savings. However, it may include introductory bonuses, so verify ongoing terms to ensure sustained returns beyond the first year.

How much can I put in an ISA each year?

You can contribute up to £20,000 to all your ISAs combined each tax year, from 6 April to 5 April, unchanged for 2025/26 according to Which?. This allowance covers cash, stocks, and Lifetime ISAs; exceeding it risks tax on excess interest. Plan contributions early, especially if transferring, to maximize tax-free growth without penalties.

What is the best fixed rate ISA for 1 year?

The top 1-year fixed rate ISA offers 4.28% AER, highlighted by Moneyfactscompare for stability. Providers like Shawbrook lock this in with minimal deposits but impose withdrawal fees. It’s best for savers confident in not needing funds soon, protecting against rate drops forecasted for late 2025.

Are ISAs still worth it in 2025?

Yes, ISAs remain valuable in 2025 due to tax-free interest up to 4.92% AER on top deals from Tembo, outpacing taxable accounts for higher earners. With personal savings allowance at £1,000 for basics, ISAs shield more. Amid economic uncertainty, their FSCS protection and growth potential make them essential for UK savers.

What are the best ISA rates for over 50s?

Best ISA rates for over 50s include 4.2% AER easy access from Nationwide’s senior accounts, building on general rates with age perks. These cater to retirement planning, often penalty-free. Compare via Martin Lewis advice for bonuses; tax benefits amplify as income rises in later years.

How do cash ISAs work?

Cash ISAs function like savings accounts but with tax-exempt interest, allowing deposits up to £20,000 yearly. Interest compounds daily or monthly at AER, paid tax-free. Governed by FCA rules, they’re FSCS-protected; choose types based on access needs to align with your financial goals.