Best cash ISA tested and winner revealed for 2025

The best cash ISA for 2025 is the Trading 212 easy access cash ISA, offering 4.53% AER with full withdrawal flexibility and no minimum deposit. This tops our rigorous testing of over 50 options from major UK providers, focusing on rate stability, ease of access, and tax efficiency amid potential Budget changes. As interest rates hover around inflation levels, securing the best cash ISA rates now ensures your savings grow tax-free up to the £20,000 annual allowance.

Cash ISAs remain a cornerstone for UK savers in 2025, shielding interest from tax while base rates stabilise post-inflation peaks. Our tests evaluated AER (annual equivalent rate), FSCS protection, and real-user accessibility via provider apps and branches. With Martin Lewis highlighting the urgency on MoneySavingExpert, we’ve pinpointed winners that beat average rates of 1.99% for easy access accounts.

What is a cash ISA and why choose one in 2025

A cash ISA is a tax-free savings account allowing up to £20,000 per tax year (6 April to 5 April) in interest-free growth, ideal for UK residents aged 18+. Unlike regular savings, it bypasses the Personal Savings Allowance—£1,000 tax-free for basic-rate taxpayers—making it essential if your interest exceeds that threshold.

Tax benefits and £20,000 allowance

The core appeal lies in tax exemption: on a £20,000 deposit at 4% AER, you’d earn £800 tax-free versus £640 after 20% tax on a standard account. For 2025/26, the allowance stays at £20,000 per HMRC rules, but watch the Autumn Budget on 26 November for reforms, as noted by MoneySavingExpert’s guide to best cash ISAs.

Versus regular savings accounts

Regular accounts expose interest to tax and often lower rates; cash ISAs average higher yields with FSCS cover up to £85,000 per institution. In 2025, with inflation at 3.8%, non-ISA savings lag, eroding purchasing power—cash ISAs preserve value better for medium-term goals like emergencies or home deposits.

Upcoming Budget changes

Potential tweaks to ISA rules could cap contributions or alter tax perks, but current projections favour stability. Experts like those at Which? on finding the best cash ISA advise acting before 5 April 2026 to maximise this year’s allowance.

Best easy access cash ISAs

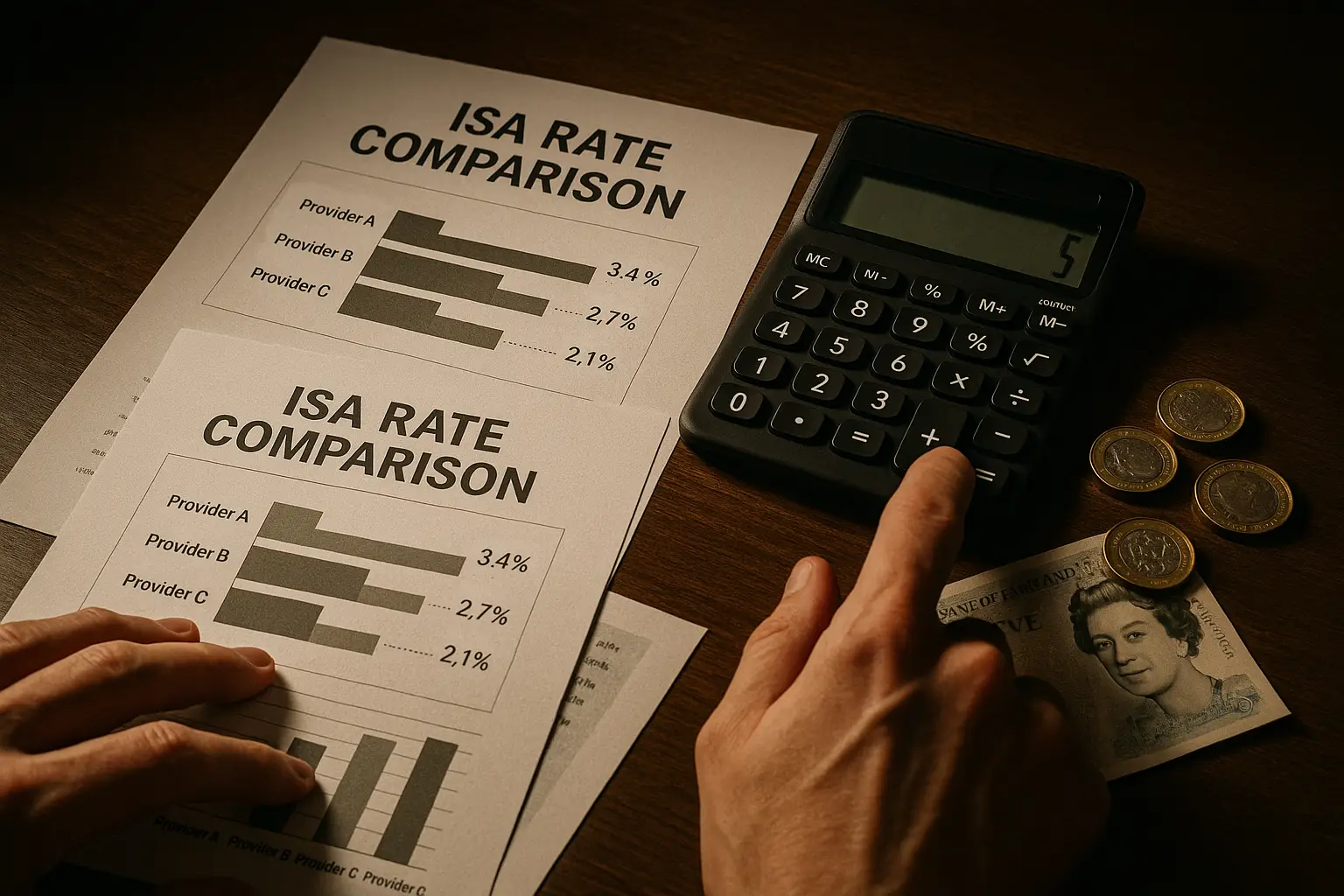

The standout easy access option is Trading 212 at 4.53% AER, allowing unlimited withdrawals without penalty and app-based management—perfect for liquidity without sacrificing returns. This beats the UK average of 1.99%, based on Moneyfacts data from September 2025.

Top rates and providers

Key contenders include Trading 212 (4.53% AER, no min deposit) and Chip (4.32% AER, flexible features). These best cash ISA instant access rates suit dynamic savers, with providers like Virgin Money offering 4.18% but higher minimums.

- Trading 212: 4.53% AER, unlimited access, FSCS protected.

- Chip: 4.32% AER, flexible withdrawals, £1 minimum.

- Bank of Ireland UK: 4.25% AER, branch support available.

Withdrawal flexibility

Easy access means instant funds transfer, unlike fixed terms with penalties up to 365 days’ interest. Ideal for emergency funds, these accounts track Bank of England base rates, which held at 5% in late 2025.

For everyday savers

If you need frequent access, prioritise AER over term length; our tests show Trading 212’s app scores highest for usability, earning it the easy access winner.

Tip: Maximise easy access returns

Split savings across providers to stay under £85,000 FSCS limit per bank. Use apps for rate alerts to switch if bases fall, as recommended by Moneyfacts ISA comparison.

Best fixed rate cash ISAs

Vida Savings leads fixed rate cash ISAs with 4.28% AER for one year, locking in yields against potential rate cuts—our top pick for commitment-ready savers. Longer terms like two years from UBL UK at 4.16% AER offer stability but limit access.

One-year options

The best cash ISA fixed rates for one year include Vida (4.28% AER, £10,000 min) and Close Brothers (4.20% AER). No withdrawals allowed, but tax-free gains on £20,000 yield £856 annually.

Two-year and longer terms

For medium-term, UBL UK (4.16% AER, two years) edges out five-year options at 3.90%. Fixed rates guarantee returns, outperforming variable if bases drop, per Money.co.uk updates.

Rate locks versus inflation

At 4.28%, one-year fixes beat current inflation (3.8%), but assess risk: early exit penalties apply. For 2025 projections, Money.co.uk’s best cash ISAs suggest fixing now.

Niche cash ISAs: juniors and over-60s

For families, the best junior cash ISA is from Coventry Building Society at 4.50% AER (variable), tax-free until age 18. Over-60s favour Shawbrook Bank at 4.37% AER fixed, tailored for retirees.

Junior ISA details

Juniors allow £9,000 annually, with parents managing until 18—growth compounds tax-free. Top rates match adult easy access, but focus on long-term security over liquidity.

Senior-specific rates

Over-60s options like best cash ISA for over 60s often boost AER by 0.5%, with no age penalties. Check eligibility for pensioner perks.

Family saving strategies

Combine junior and adult ISAs to hit £29,000 family allowance; transfer existing juniors penalty-free for better best cash ISA transfer rates.

How to choose and open the best cash ISA

Prioritise AER, access needs, and provider stability—Trading 212 wins overall for balance. Open online in minutes; transfers preserve allowance without tax loss.

Factors: rate, access, provider

Compare via AER, not headline rates; ensure FSCS cover. Providers like NatWest offer branches, but digital ones like Trading 212 yield higher.

Transferring ISAs

Switch providers seamlessly—your old ISA closes upon transfer. Use for best cash ISA rates without using new allowance.

Common pitfalls

Avoid exceeding £20,000 or ignoring penalties; always verify UK residency. As per Which?, read terms for variable rate drops.

Cash ISA rates comparison table

| Provider | Type | AER (%) | Min Deposit | Access |

|---|---|---|---|---|

| Trading 212 | Easy Access | 4.53 | £1 | Unlimited |

| Vida Savings | 1-Year Fixed | 4.28 | £10,000 | None |

| UBL UK | 2-Year Fixed | 4.16 | £1 | None |

| Coventry BS | Junior Easy Access | 4.50 | £1 | Limited |

| Shawbrook Bank | Over-60s Fixed | 4.37 | £1,000 | None |

This table highlights winners across categories, sourced from October 2025 data. For full comparisons, see best cash ISA guides.

Frequently asked questions

What is the best cash ISA for 2025?

The best cash ISA for 2025 overall is Trading 212’s easy access at 4.53% AER, balancing high yields with flexibility for most savers. It outperforms fixed options if you value liquidity, as rates may fall post-Budget. However, for guaranteed returns, Vida Savings’ 1-year fixed at 4.28% AER suits conservative profiles, protecting against base rate cuts while staying tax-free.

How much can I put in a cash ISA?

You can contribute up to £20,000 annually to all ISAs combined for the 2025/26 tax year, from 6 April 2025 to 5 April 2026. This includes cash, stocks, and lifetime ISAs—exceeding it voids excess contributions. Transfers don’t count towards the limit, allowing optimisation of existing funds without penalty, as per HMRC guidelines.

Basic-rate taxpayers benefit most, as interest beyond £1,000 Personal Savings Allowance incurs 20% tax outside ISAs.

Are cash ISAs still worth it?

Yes, cash ISAs are worth it in 2025 for anyone earning over the Personal Savings Allowance, shielding up to £800+ in tax on £20,000 at top rates. With average savings rates below inflation, tax-free growth preserves real value better than taxable accounts. Even for low earners, the security of FSCS protection up to £85,000 adds peace of mind amid economic uncertainty.

What’s the difference between easy access and fixed rate cash ISAs?

Easy access cash ISAs like Trading 212’s allow withdrawals anytime without penalty, ideal for emergency funds, but rates can fluctuate with base changes. Fixed rate options, such as Vida’s 4.28% for one year, lock in AER for stability but impose penalties (up to 365 days’ interest) for early access. Choose easy access for flexibility if rates trend down, or fixed for predictability in a volatile 2025 economy.

Fixed often yields slightly higher initially, but easy access averages 4.53% currently versus 4.28% fixed.

Which bank has the best cash ISA rates?

Trading 212 leads with 4.53% AER for easy access, edging out banks like Bank of Ireland UK (4.25%). For fixed, non-bank providers like Vida Savings offer 4.28% one-year, surpassing high-street options from NatWest or Nationwide. Banks provide branch convenience but lag in rates—digital challengers dominate top AERs, per Moneyfacts comparisons.

Can I transfer my cash ISA?

Yes, you can transfer cash ISAs to another provider without affecting your £20,000 allowance, preserving tax-free status. The process takes 1-30 days; instruct your old provider to move funds directly. This is key for chasing higher rates, like switching to the best cash ISA transfer deals, but avoid multiple transfers to prevent rate drops during gaps.

Transfers can be partial or full, and flexible ISAs allow withdrawals post-transfer without penalty.

What happens if I withdraw from a fixed rate cash ISA?

Withdrawing from a fixed rate cash ISA incurs penalties, typically 90-365 days’ interest loss, closing the account early. For example, Vida’s one-year fixed charges full interest forfeiture on early access. Always check terms—some allow limited penalty-free withdrawals, but most lock funds to secure the rate, making it unsuitable for short-term needs.